Since you cannot predict the future I recommend not waiting “for prices to drop”.

Instead, buy a house when you find one you love and that you can afford. Houses are not widgets- each have pluses and minuses and optimizing for price won’t make you happy.

If somebody bought early this year, they may be trapped in their home with negative equity for a decade, like many were after 2008.

Your advice is mostly sound, but buying in a bubble can have severe and very real ramifications on you, even if you can afford the monthly payment. You may not be able to move without writing the bank a large check, and many won’t have the cash on hand

You seem to be looking at buying a house as an investment. I'd argue otherwise: your first piece of real estate is a necessity, not an investment - you always need a place to live. So, in financial terms, you're closing a short position, not opening a long position.

Of course there is non-negligible friction if you need to move, so you do want to be mindful of not buying right at the peak, but in general I think you're overstating how much you need to worry about prices: you don't profit when prices go up, since you'd also have to pay more for a new place, and as long as you can afford the payments, your home moves in line with the market and don't need to sell, you also don't need to let falling prices affect your sleep. Your position is market neutral, you are mostly giving up flexibility.

While I think you're right in ordinary times, this doesn't work during a bubble. You could be totally blocked from moving if your home is worth a fraction what you owe on it, no matter how necessary the move is (job, school district, family).

Even then there are some mitigants: you could try to rent out your first home and rent or even buy a new one. Tax-wise that would work against you (usually, in most places), but it probably wouldn't bankrupt you.

I agree, of course you don't want to have bought right before a dip. But if you sketch out a few scenarios and look at the overall and your individual situation (eg, Would rental income cover credit payments, even in an adverse scenario? Do you have expenses you could claim in years when you're renting out? Do you have other uses for the property, eg within a family?), you might find that you can manage the risk (or not). It's definitely not risk-free, but there's also significant upside potential if you can make a long-term commitment.

He might be thinking of people in the US who are not in Alaska, Arizona, California, Connecticut, Idaho, Minnesota, North Carolina, North Dakota, Oregon, Texas, Utah or Washington.

In those states first mortgages are "non-recourse" loans. What that means is that if the borrower does not pay off the loan the lender's remedy is limited to whatever they can get foreclosing and then selling the house.

With a non-recourse loan if I find myself owing a lot more on my mortgage than my house is worth I've got the option of just walking away and letting the lender foreclose. I will no longer have a house after that, but my possessions and savings and investments and income will be safe.

In the other states first mortgages might be "recourse" loans. With those if selling the house isn't enough to pay off the loan they can come after you personally for the difference.

With a recourse loan the lender can come after me for the shortfall if the foreclosure sale isn't enough to pay off the loan. They might go after my possessions, saving, investments, and income.

Most people are putting down 20%. Even if you have a non-recourse loan that's a huge loss. Plus the hit to credit record means you probably won't be able to take out a new mortgage for years.

It'd only be a tiny percent of people who found themselves underwater, but with so little equity they didn't care to lose it, and who also didn't care about tanking their credit score for the next decade.

> You seem to be looking at buying a house as an investment. I'd argue otherwise: your first piece of real estate is a necessity, not an investment - you always need a place to live.

You need housing, but you can get that without home ownership.

I wish it was that clear cut. Here in Australia there is an acute shortage of rentals and rents are going through the roof [0]. As with everything, there is always a caveat.

Usually you cannot, but the fed has expressly told us they will be raising interest rates. They could be lying, but I think this is one of the few times you can "predict the future" and expect rising interest rates to influence demand.

But long term treasury yields are now lower than short term treasury yields. This indicates that the market expects inflation and interest rates to drop in the future. As long as this is true, prices for houses will not go down as everyone assumes that a refi will be possible in 1-2 years. Housing market will be stuck while this sorts itself out.

You can’t refi with negative or low equity, as most who bought in the last year are likely to have.

If inflation does come down rapidly, it’s likely to be coupled with a sharp increase in unemployment.

Rates fell significantly from 2005 to 2012, yet housing continued to fall. Whether lower rates or higher unemployment is the stronger force this time remains to be seen.

Given housing is by far at a historical peak in real terms, I suspect a reversion to the mean in real prices is more likely than not

> This indicates that the market expects inflation and interest rates to drop in the future.

It indicates that the market thinks the Fed will be effective. It's also (generally) indicative that a recession is on the horizon. We're starting to see the layoffs in certain sectors (tech especially). Unemployment rising tends to cause more mortgage defaults which will tend to lower home prices.

> As long as this is true, prices for houses will not go down as everyone assumes that a refi will be possible in 1-2 years.

A lot of potential buyers don't qualify at current (and rising) rates. They've been taken out of the market entirely. Wells Fargo saying that applications for new mortgages are down 90%. Assuming that's happening industrywide (no reason to doubt that) it's going to start effecting prices - and already is in some markets.

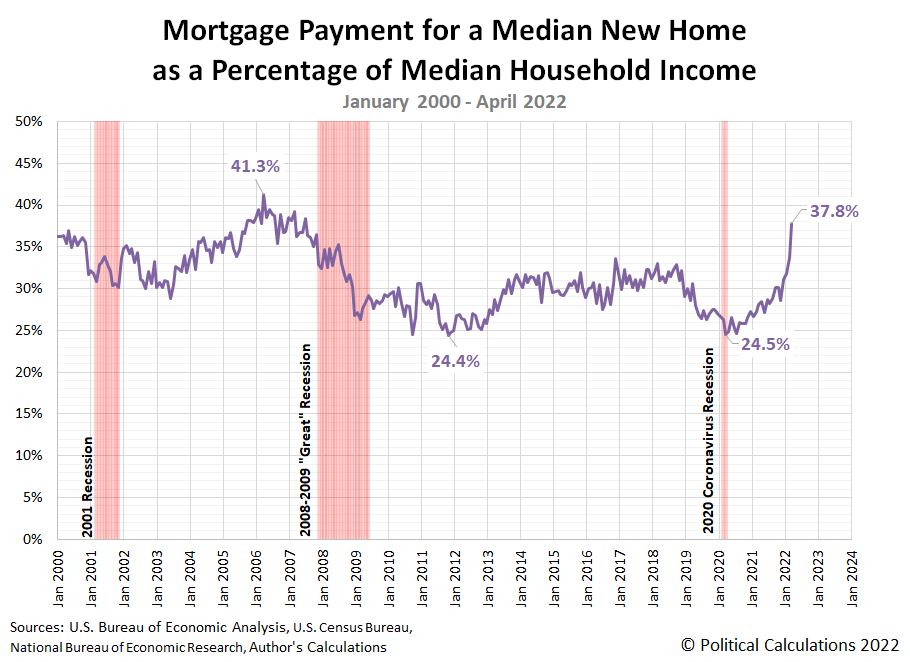

This is the chart I am referring to concerning mortgage payments, which IMO have remained within 10 percentage points of where they've been since 2000:

There is a sharper rise now of higher payments, but historically its not even where it was in 2006 and still is lower than figures not seen in this present chart, like the the 1980s.

In the end home prices don't march up in a vacuum, the money has to come from somewhere. People pay these prices and they can do so because they are skilled workers who are paid such incomes to afford homes in the Bay area or Boston or other high cost of living areas. It's not all private equity. When you add more high income jobs to an area than units of housing for decades, a housing crisis for the working class is the natural result, but for high income earners they will always be paid enough to afford the median mortgage payment or else the median will shift accordingly to meet the market where it is.

> Since you cannot predict the future I recommend not waiting “for prices to drop”.

This is questionable advice, and biased I guess.

It's quite easy to review historical sale data and see if a person is buying at a peak price. No it likely won't be the only or final peak, but it's a useful indicator.

> optimizing for price won’t make you happy.

On the other hand, not optimizing for price can make you significantly unhappy. Being immobilized due to an upside down mortgage, and stretching monthly finances can be really stressful.

{kind=link}

Since you cannot predict the future I recommend not waiting “for prices to drop”.

Instead, buy a house when you find one you love and that you can afford. Houses are not widgets- each have pluses and minuses and optimizing for price won’t make you happy.